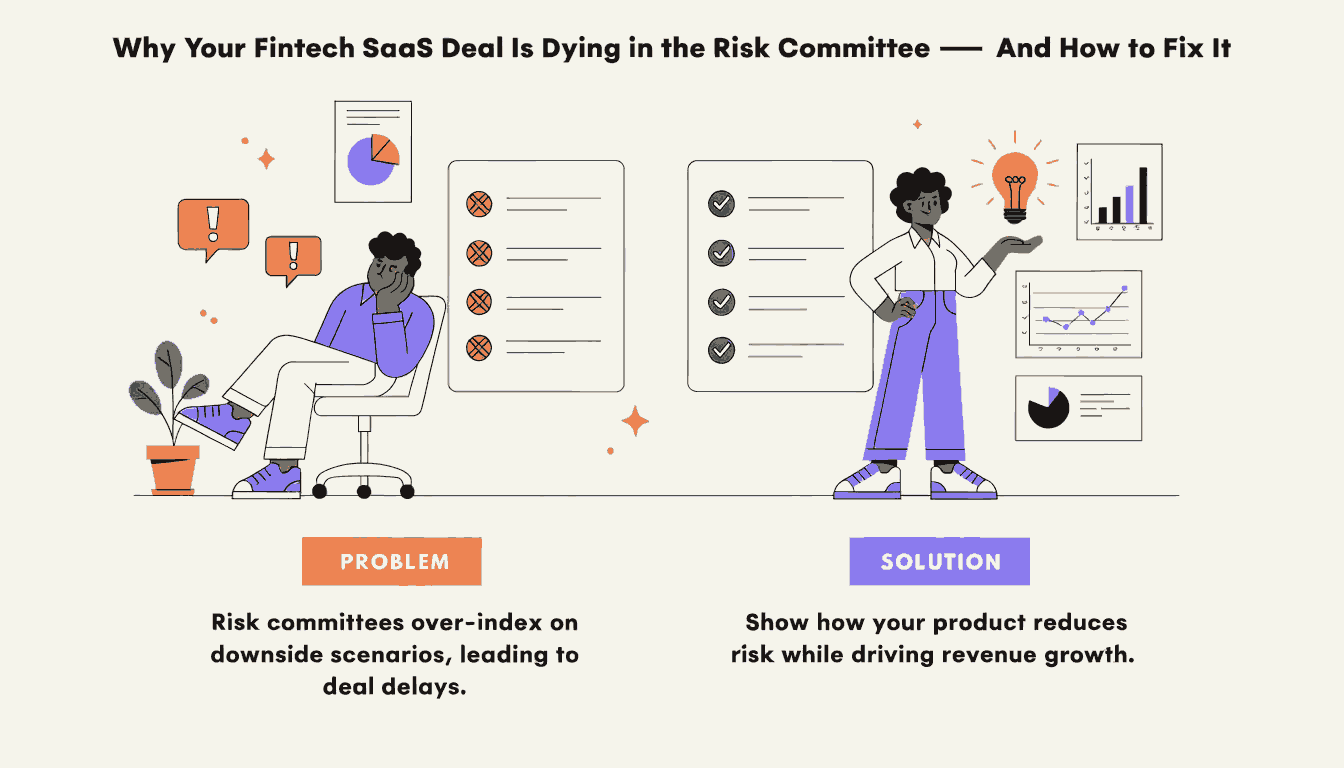

Why Your Fintech SaaS Deal Is Dying in the Risk Committee — And How to Fix It

By Gaurav Rao 27-05-2026 62

Closing enterprise deals in fintech is no longer only about product features, pricing, or innovation. Many fintech SaaS companies in India spend months building relationships, running demos, and negotiating commercial terms—only to see deals suddenly stall at the final stage.

More often than not, the problem is not the product.

The problem is the risk committee.

Across banks, NBFCs, insurers, and regulated financial institutions, internal risk and compliance teams are becoming increasingly influential in software purchasing decisions. A fintech solution may impress operational teams, but if compliance, security, legal, or governance stakeholders are unconvinced, the deal can quietly die before approval.

This shift is fundamentally changing enterprise fintech sales.

Today, winning large financial clients requires more than strong technology. It requires demonstrating trust, governance maturity, security readiness, and regulatory alignment.

This is why Fintech SaaS and Compliance-Aware Authority is becoming one of the biggest differentiators for B2B fintech companies in India.

Why Risk Committees Have Become So Powerful

Financial institutions operate in highly regulated environments.

Banks and NBFCs are responsible for:

- Customer data protection

- Financial security

- Regulatory compliance

- Fraud prevention

- Vendor governance

- Operational resilience

A bad vendor decision can create:

- Regulatory penalties

- Data breaches

- Reputation damage

- Operational disruption

- Legal exposure

As a result, risk committees now play a major role in evaluating third-party technology providers.

Even if business teams love your platform, risk stakeholders may block approval if they see:

- Weak compliance posture

- Poor security governance

- Inadequate documentation

- Limited audit readiness

- Unclear data handling practices

Enterprise fintech sales are increasingly trust-driven rather than feature-driven.

Your Product Is Not the Only Thing Being Evaluated

Many SaaS founders assume clients are only assessing:

- Product functionality

- User experience

- Pricing

- Integrations

- Automation capabilities

In reality, risk teams are evaluating your entire company.

They want to understand:

- Who runs the company

- How data is secured

- Whether governance processes exist

- How incidents are managed

- Whether vendors are audited

- How customer information is stored

- What compliance controls are in place

In many cases, the perceived operational maturity of your organization matters as much as the software itself.

Compliance Is Becoming a Revenue Function

Historically, compliance was treated as a back-office responsibility.

That mindset is changing rapidly.

For fintech SaaS companies, compliance readiness is now directly connected to:

- Enterprise sales velocity

- Procurement approvals

- Partnership opportunities

- Customer trust

- Market credibility

A weak compliance posture can slow down:

- Security reviews

- Legal negotiations

- Vendor onboarding

- Procurement approvals

In some cases, deals collapse entirely because startups underestimate enterprise risk expectations.

Why Indian Financial Institutions Are More Cautious Today

India’s financial ecosystem is experiencing rapid digital transformation.

At the same time, institutions are facing rising concerns around:

- Cybersecurity threats

- Data privacy

- Third-party risk

- AI governance

- Fraud prevention

- Regulatory scrutiny

The Digital Personal Data Protection Act, 2023 has further increased accountability around personal data handling.

Banks and NBFCs are now expected to exercise stronger oversight over vendors processing sensitive customer information.

This means fintech SaaS providers are increasingly evaluated through a compliance and governance lens.

Common Reasons Fintech Deals Fail in Risk Committees

Weak Security Documentation

Many startups lack structured security policies, audit reports, or governance frameworks.

Risk teams expect documentation around:

- Access controls

- Encryption

- Incident response

- Data retention

- Vendor management

Without this, trust declines quickly.

Poor Data Governance Clarity

Financial institutions want to know:

- Where data is stored

- Who can access it

- How long it is retained

- Whether third parties are involved

Unclear answers create immediate concern.

Lack of Compliance Certifications

Enterprise buyers often expect evidence of:

- ISO standards

- Security audits

- Compliance assessments

- Penetration testing

Startups without structured validation may appear risky.

Founder-Led Informality

Many early-stage startups operate with highly informal processes.

While this may work internally, enterprise clients often interpret operational informality as governance weakness.

No Enterprise Risk Narrative

Many SaaS companies explain features well but fail to communicate:

- Risk mitigation

- Regulatory awareness

- Governance maturity

- Operational accountability

Risk committees need reassurance, not just innovation.

Procurement Is Increasingly About Trust Signals

Enterprise buyers increasingly evaluate external trust signals before approving vendors.

These may include:

- Leadership credibility

- Security transparency

- Public documentation

- Customer references

- Case studies

- Governance maturity

- Industry reputation

Fintech SaaS companies that proactively demonstrate credibility create smoother procurement experiences.

Trust signals reduce uncertainty.

Why Founder Visibility Matters in Enterprise SaaS

In B2B fintech, buyers often evaluate the leadership team behind the company.

Risk stakeholders want confidence that founders:

- Understand financial regulations

- Take compliance seriously

- Can handle enterprise responsibilities

- Will remain accountable long term

Strong founder visibility can improve credibility significantly.

This includes:

- LinkedIn presence

- Industry commentary

- Public expertise

- Conference participation

- Thought leadership

- Transparent company communication

Enterprise trust increasingly extends beyond the product itself.

Security Pages and Trust Centers Are Becoming Essential

Modern fintech SaaS companies increasingly build dedicated:

- Security pages

- Compliance centers

- Trust portals

- Governance documentation hubs

These pages help answer common enterprise concerns proactively.

A strong trust center may include:

- Security practices

- Compliance standards

- Data handling policies

- Infrastructure details

- Incident response commitments

- Privacy frameworks

This reduces procurement friction and accelerates risk evaluations.

Sales Teams Must Learn Compliance Language

One major issue is that many fintech sales teams speak only in product language.

Risk committees speak a different language focused on:

- Governance

- Controls

- Accountability

- Security

- Auditability

- Risk mitigation

SaaS companies that align messaging with enterprise risk expectations perform better during procurement reviews.

For example:

Instead of saying:

- “We automate workflows”

you may also need to explain:

- “We maintain audit logs, role-based access controls, and secure permission governance.”

Compliance-aware communication improves enterprise confidence.

AI Adoption Is Increasing Risk Scrutiny

As fintech platforms adopt AI-powered systems, risk evaluations are becoming even stricter.

Financial institutions now ask questions about:

- AI explainability

- Data usage

- Model governance

- Bias controls

- Security oversight

- Human review mechanisms

Fintech companies using AI without clear governance frameworks may face stronger resistance from procurement teams.

Enterprise Buyers Want Long-Term Stability

Risk committees are not only evaluating current capabilities.

They also evaluate whether your company appears stable enough for long-term partnership.

This includes:

- Operational maturity

- Leadership consistency

- Governance structures

- Compliance investment

- Infrastructure scalability

Enterprise buyers avoid vendors that appear operationally fragile.

How Fintech SaaS Companies Can Fix the Problem

Build a Compliance-First Narrative

Position your company as security-conscious and governance-aware from the beginning.

Create a Dedicated Trust Center

Publish clear documentation around:

- Security

- Compliance

- Privacy

- Infrastructure

- Governance practices

Invest in Certifications and Audits

Independent validation improves enterprise confidence significantly.

Improve Founder Authority

Founders should actively build industry credibility and demonstrate expertise publicly.

Train Sales Teams on Risk Communication

Enterprise sales teams should understand procurement and compliance concerns deeply.

Document Governance Processes

Even startups need:

- Incident response procedures

- Access controls

- Vendor governance

- Data management policies

Operational maturity matters.

The Future of Fintech SaaS Sales Is Compliance-Led

India’s fintech ecosystem will continue growing rapidly, but enterprise procurement expectations are also rising.

Banks, NBFCs, and insurers are becoming more selective about:

- Vendor governance

- Security maturity

- Compliance readiness

- Operational accountability

In this environment, the companies that win will not necessarily be those with the most features.

They will be the companies that inspire the most trust.

Fintech SaaS businesses that proactively invest in governance, transparency, and compliance-aware authority will close deals faster, build stronger partnerships, and create long-term enterprise credibility.

In modern fintech sales, compliance is no longer just a legal requirement.

It is becoming one of the strongest growth drivers in the industry.

FAQs:

1. Why do fintech SaaS deals fail in risk committees?

Deals often fail due to weak compliance readiness, poor security governance, unclear data handling practices, or lack of enterprise trust signals.

2. What does a risk committee evaluate in fintech procurement?

Risk committees assess security, governance, compliance, operational maturity, vendor stability, and data protection practices.

3. Why is compliance important in enterprise fintech sales?

Compliance reduces procurement risk and helps enterprise buyers trust fintech vendors handling sensitive financial data.

4. How does the DPDP Act affect fintech SaaS companies?

The Digital Personal Data Protection Act, 2023 increases accountability around personal data handling and vendor oversight.

5. What are enterprise trust signals?

Trust signals include certifications, security documentation, founder credibility, case studies, governance practices, and compliance transparency.