Why Waiting for the "Perfect Time" Never Works

There's this excuse that people make a lot. I would begin saving as soon as I make more money. Or perhaps, I must get this loan off my hands and then consider making an investment. Sounds familiar? The trouble with waiting is that the perfect moment never does. Life keeps throwing in new expenses, new desires, new causes for postponing. Meanwhile, years slip by. The truth nobody likes hearing is this: someone who started putting away ₹3,000 monthly five years ago is probably better off today than someone earning double but still planning to start "soon." Monthly savings isn't about having loads of spare cash. It's about deciding that future security matters enough to begin now, even with whatever little is available.

Getting Real About Where Money Actually Disappears

Most people genuinely believe they know their spending patterns. Then they actually track expenses for a month and get shocked. Those weekend coffees? Add up to ₹2,500. Impulse online shopping during sales? Another ₹4,000 gone. Subscription services barely used? ₹1,200 more. Suddenly the mystery "where does my salary vanish" gets solved. The following is a simple method that should work: For a period of one month, just one month, record every single expense. Yes, even that ₹20 for parking. Use a phone app, a notebook, whatever. At month-end, the patterns become obvious. Some expenses are non-negotiable like rent and groceries. Others? Pure habit. Cutting down does not mean living miserably. It means choosing consciously. Maybe by cooking twice in a week you save Rs. 3000. Maybe cancelling unused gym memberships frees up the Rs.1500. That's 4500/- per month or 54,000/- per year ready for better use. When Calculators Become Your Best Friends

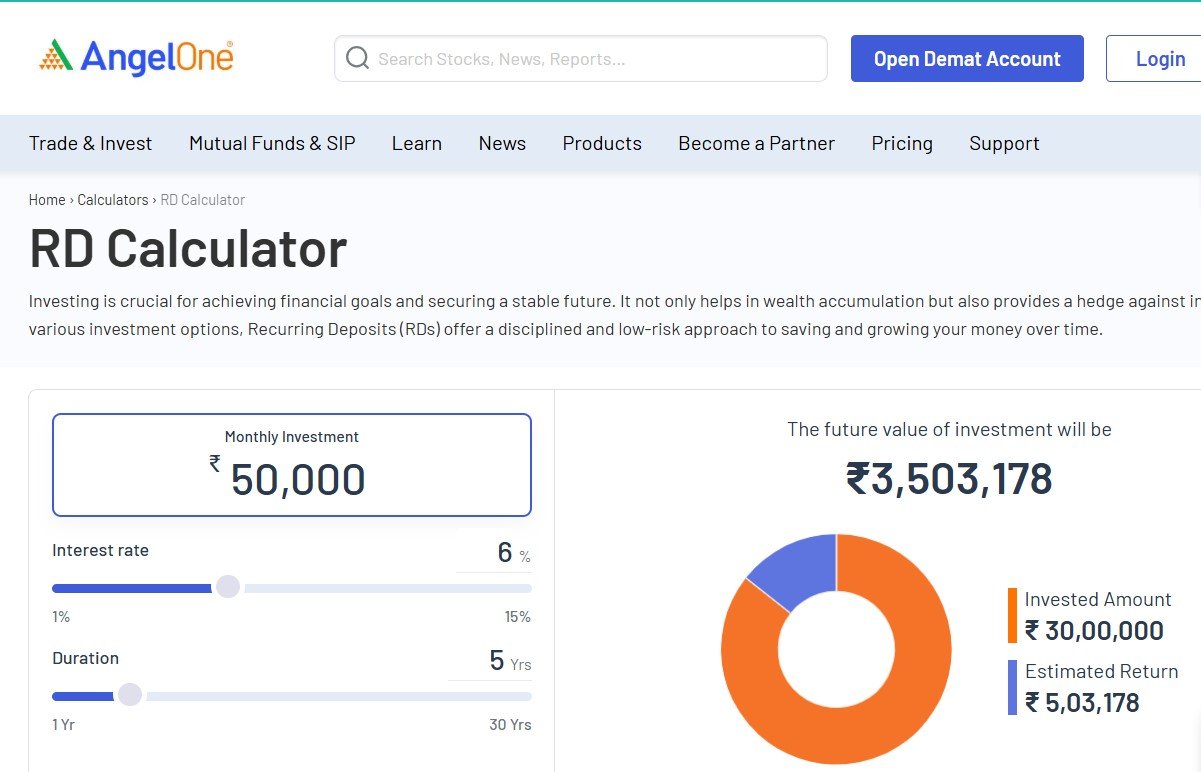

Technology has made financial planning ridiculously easy compared to what our parents dealt with. Take the SIP calculator, for example. This simple tool answers the question everyone wonders about: "If I invest this much every month, what will I actually have later?" No guessing, no complicated maths. Just enter three things. How much can you invest monthly? For how many years? What returns do you expect (usually 10-12% for equity funds)? Within seconds, the answer appears. Planning ₹8,000 monthly for 15 years expecting 12% returns? The calculator shows the final corpus, total amount invested, and returns earned separately. It's eye-opening, really. Similarly, the RD calculator helps with recurring deposits. These work differently from mutual funds because returns are fixed and guaranteed. Someone preferring safety over higher returns loves RDs. Both calculators let people experiment. What if I increase the monthly amount after five years? What if I extend the duration? Playing with these numbers until finding a comfortable fit makes planning feel less scary and more achievable.

The Safety Net and Growth Engine Strategy

Here's something financial advisors won't always say upfront: putting all savings in one place is foolish. Doesn't matter if it's all in mutual funds or all in fixed deposits. Balance matters. Think of it like this. Life throws curveballs. Medical emergencies, suddenly losing their jobs, home repairs that need to be taken care of. For these situations, money needs to be accessible immediately and without risk. This is where recurring deposits or fixed deposits work brilliantly. Keep at least six months of expenses in such safe instruments. Consider it the monetary cushion to peacefully sleep at night. Now, of course, for longer-term objectives, such as retirement, children's education or buying property, recurring deposits won't cut it. Inflation chomps away at those meagre returns. This is where Systematic Investment Plans in mutual funds enter. Yes, markets go up and down. But over 10, 15, 20 years, equity-oriented funds historically deliver far better returns than traditional savings. It's using both intelligently based on when the money is needed.

Making Saving Automatic Because Willpower Fails

Human beings are terrible when it comes to self-control when it comes to money. It is not being an insult that is biology. When salary hits the account and there's ₹50,000 sitting there, the brain starts calculating what can be bought. New phone? Weekend trip? That jacket on sale? Saving whatever remains at month-end rarely works because nothing remains. The solution is brutally simple: automate everything. Set up standing instructions so that on salary day, money automatically moves into SIPs or RDs before there's even a chance to see it. What's left becomes the spending budget. Sounds restrictive? Actually, it's liberating. There's zero guilt about spending what remains because savings already happened. Start small if needed. Even ₹1,000 monthly is fine initially. The amount matters less than building the habit. As income grows or expenses reduce, increase the automated amount. Before long, saving becomes as natural as paying rent.

Life Changes, Plans Should Too

Nobody's life stays static. Five years ago, someone might have been single with zero responsibilities. Ten years later, kid's education becomes priority. Another decade, retirement planning takes centre stage. Financial plans pretending these changes won't happen are destined to fail. The smart approach involves reviewing everything at least twice yearly. Maybe every January and July. Ask hard questions. Are the current investments still aligned with goals? Has income increased enough to boost monthly contributions? Do new responsibilities require adjusting the safety fund? This is where those RD calculator and SIP calculator prove useful again. Quickly check how increasing the SIP amount by ₹3,000 changes the final outcome. Or how adding three more years to the investment period impacts returns. Sometimes tiny adjustments make massive differences. Someone who invests Rs.5,000 a month may find that increasing it to Rs.7,000 gets him there two years sooner. That's powerful information. Plans shouldn't be rigid documents gathering dust. They're living strategies that evolve alongside actual life.

Tags : RD calculator