Digital Loan Origination vs Traditional Lending: What Every Modern Lender Must Know

For decades, lending in India followed the same playbook. A borrower walked into a branch, filled out a paper form, submitted physical documents, and then waited — sometimes weeks — for a credit officer to manually review the file and issue a decision. This was traditional lending: slow, labour-intensive, relationship-driven, and deeply human.

Then came digital loan origination — and everything changed.

Today, a borrower can apply for a loan from their smartphone in under five minutes, receive an automated credit decision in seconds, sign a digital agreement, and have funds in their account before lunch. The gap between these two experiences is not merely technological; it represents a fundamental shift in how lending businesses are built, scaled, and competed on.

For NBFCs, banks, MFIs, and fintech lenders in India, understanding this shift is not optional. It is the defining strategic question of the decade. This article breaks down the head-to-head comparison across every dimension that matters — and shows how Roopya's platform is built for lenders who have chosen the digital future.

1. What Is Digital Loan Origination?

Digital loan origination is the process of capturing, evaluating, and processing a borrower's loan application entirely through automated digital systems — with little to no manual intervention. It encompasses everything from the initial borrower-facing application form to automated KYC, credit bureau pulls, AI-powered document analysis, instant credit decisioning via a Business Rule Engine (BRE), digital offer delivery, eSign, and disbursement trigger.

Platforms like Roopya make digital loan origination accessible to lenders of all sizes — not just large banks with multi-crore IT budgets. Through pre-built integrations, no-code configuration, and a pay-as-you-use model, an NBFC can run a fully digital origination operation from day one.

2. What Is Traditional Lending?

Traditional lending refers to the branch-based, document-heavy, manually operated model that has characterised Indian lending for generations. Applications arrive on paper or via email. Credit officers manually verify documents, call references, and apply judgement-based underwriting. Decisions are made in credit committee meetings. Agreements are printed, couriered, signed in wet ink, and stored in physical files.

Traditional lending is not inherently bad — it served millions of borrowers for decades. But in today's market environment, it carries serious structural disadvantages that compound over time.

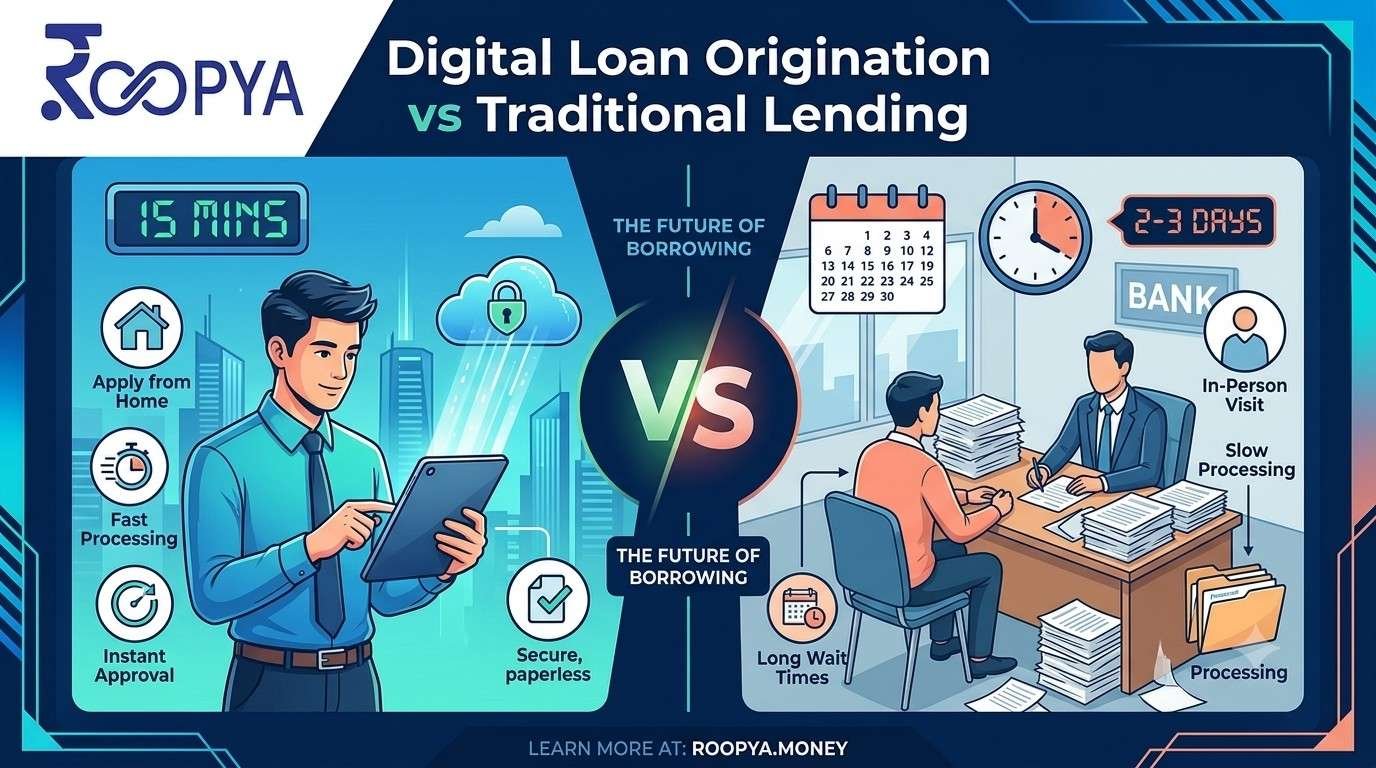

3. Speed: Seconds vs. Weeks

This is the most visible difference between digital loan origination and traditional lending, and it is staggering in its magnitude.

In a traditional lending workflow, the application-to-sanction cycle typically ranges from 5 to 21 working days. Document collection, physical verification, manual underwriting, credit committee review, and agreement printing all consume time in sequence. Each handoff between teams introduces delay. Errors in a paper application can restart the entire process.

In a digital origination workflow on a platform like Roopya, clean-profile applications can go from submission to sanction in under 15 minutes. KYC is triggered automatically. Bureau reports are pulled in real time. AI analyses uploaded documents within seconds. The BRE evaluates the application against your credit policy instantly. A personalised loan offer is generated and delivered without human intervention.

For borrowers comparing lenders in real time — as most digital-first borrowers do — this speed difference is not a preference; it is the deciding factor. The lender that responds in minutes wins; the lender that responds in days is forgotten.

4. Cost Per Loan: Efficiency at Scale

Processing a loan application manually is expensive. A traditional lender must maintain branch infrastructure, employ credit officers, fund document storage, manage courier logistics, and absorb the cost of human error and rework. Industry estimates suggest the cost to process a single loan application manually in India ranges from ₹1,500 to ₹4,000, depending on product complexity and geography.

Digital loan origination dramatically compresses this cost. Automated KYC, AI document processing, and instant credit decisioning eliminate the largest cost line items. On Roopya's platform, lenders consistently report cost-per-application reductions of 40–60% versus their previous manual workflows. As volume scales, the savings compound — because digital systems do not require proportional headcount growth.

The cost difference creates a structural competitive advantage. Digital lenders can offer more competitive rates, wider credit access, and higher marketing spend — all while maintaining better margins than their traditional competitors.

5. Accuracy and Consistency: Machine Precision vs. Human Variability

Manual underwriting introduces variability by design. Two credit officers reviewing the same application may reach different conclusions. Fatigue, cognitive bias, inconsistent interpretation of credit policy, and simple data entry errors all degrade the quality of traditional lending decisions.

Digital loan origination solves this problem at the root. When a Business Rule Engine applies your credit policy to every application, the rules are executed identically every single time — regardless of volume, time of day, or staff availability. AI-powered document analysis extracts data with 99%+ accuracy. Bureau scores are pulled and interpreted through standardised algorithms. The result is a credit decision that perfectly reflects your policy, every time.

Roopya's no-code BRE allows credit and risk teams to configure, test, and update underwriting rules independently — without developer involvement. When regulatory changes or portfolio insights require a policy update, it can be implemented in minutes, and the new rules go live immediately across every application in the queue.

6. Customer Experience: Friction vs. Delight

Traditional lending was designed around the lender's operational convenience, not the borrower's experience. Branch hours, document collection appointments, waiting rooms, and phone follow-ups are all friction points that borrowers tolerate only because they have no alternative. In a market where they do have alternatives, they simply leave.

Digital loan origination is designed around the borrower. Applications are available 24/7 from any device. Smart forms pre-fill data where possible and validate inputs in real time. KYC is completed in under two minutes via Aadhaar eKYC. Loan decisions are instant. Offer letters arrive on screen — not via post. eSign takes seconds. The entire experience can be completed without speaking to a single person.

This matters enormously for conversion rates. A frictionless digital application journey significantly outperforms traditional branch-based intake on every metric — application completion rates, time to acceptance, and borrower satisfaction scores. Roopya's borrower journeys consistently deliver high completion and satisfaction rates, with applicants regularly citing speed and simplicity as the top reasons they would recommend the lender to others.

7. Compliance and Audit: Digital by Design

Regulatory compliance is an area where traditional lending is structurally vulnerable. Paper-based processes make it difficult to produce consistent audit trails. Physical document storage creates data security risks. Manual KYC verification is prone to gaps. Credit bureau reporting requires dedicated reconciliation effort.

Digital loan origination, by contrast, generates a complete, immutable digital audit trail automatically. Every action — who accessed the application, what data was checked, what decision was made and why, when each step occurred — is logged in real time. Consent management is built into the borrower journey. Bureau reporting happens automatically. RBI examination requirements can be met through software-generated reports rather than manual file pulling.

Roopya's platform is continuously updated for RBI compliance, ensuring that lenders on the platform are always aligned with current regulatory requirements — without needing to monitor and implement regulatory changes themselves.

8. Scalability: The Exponential Advantage

This is where the long-term strategic implications of digital loan origination become most clear. A traditional lending operation scales linearly: double your application volume, and you need roughly double the staff, double the branch space, double the document storage.

A digital lending operation on a cloud-native platform like Roopya scales exponentially. The same infrastructure that processes 500 applications a month can handle 50,000 applications a month — with no additional headcount, no new branches, and no proportional cost increase. The platform scales automatically, handling demand spikes without degradation.

This scalability asymmetry means that digital lenders can pursue growth opportunities — new geographies, new product lines, new borrower segments — that traditional lenders cannot access profitably.

9. The Verdict: Why Digital Loan Origination Wins

The comparison is not close. Digital loan origination outperforms traditional lending across every dimension that matters to a modern lender — speed, cost, accuracy, customer experience, compliance, and scalability.

Traditional lending is not disappearing overnight. Complex credit products, relationship-based lending to large corporates, and certain underserved markets will continue to involve human judgement for years to come. But for the vast majority of retail and MSME lending — personal loans, business loans, microfinance, gold loans, vehicle loans — the digital model is definitively superior.

The question for lenders in India today is not whether to make the transition. The question is how quickly, and with which platform.

10. How Roopya Makes Digital Loan Origination Accessible

Roopya is a no-code digital lending infrastructure platform purpose-built for Indian lenders. It offers the same digital origination capabilities that large banks have spent years and crores building — packaged as a ready-to-deploy, pay-as-you-use platform that any NBFC, MFI, or fintech can go live on in a single day.

- 1-Day Go-Live: Pre-built product journeys and 300+ pre-integrated APIs mean zero custom development required.

- No-Code BRE: Credit teams configure and update underwriting rules independently — no developers needed.

- AI-Powered Processing: Document OCR, fraud detection, and ML-based credit scoring built in as standard.

- Full Regulatory Compliance: Always updated for RBI requirements, with built-in audit trails and consent management.

- Pay-As-You-Use: Zero upfront costs. You grow on Roopya's infrastructure without capital expenditure.

If you are still running loan origination on manual workflows, spreadsheets, or legacy software, the competitive gap between you and digital-first lenders is widening every day. Roopya closes that gap — in 24 hours. Request a free demo at roopya.money and see what a fully digital origination operation looks like for your business.

FREQUENTLY ASKED QUESTIONS (FAQ)

Q1: What is the main difference between digital loan origination and traditional lending?

Digital loan origination automates the entire loan application process — KYC, document analysis, credit decisioning, and agreement execution — using software and AI, delivering decisions in minutes. Traditional lending relies on manual processes, physical documentation, and human underwriting, which typically takes days to weeks and involves significantly higher operational costs.

Q2: Is digital loan origination safe and RBI compliant?

Yes. Leading digital loan origination platforms like Roopya are fully compliant with RBI regulations, including KYC norms under PMLA, digital consent requirements, data localisation rules, and credit bureau reporting standards. Every step generates a complete digital audit trail, making compliance documentation simpler than in traditional manual workflows.

Q3: Can small NBFCs afford to implement digital loan origination?

Absolutely. Roopya's pay-as-you-use pricing model eliminates upfront costs, making enterprise-grade digital origination accessible to NBFCs at every stage of growth. There are no large licence fees or infrastructure costs — lenders pay only for what they actually process, and go live in a single day without custom development.

Q4: How much faster is digital loan origination compared to traditional lending?

A clean-profile application processed on Roopya's digital origination platform can move from submission to sanction in under 15 minutes. The equivalent traditional lending process — including manual document review, credit committee evaluation, and physical agreement execution — typically takes between 5 and 21 working days.

Q5: Does switching to digital loan origination require replacing my entire team?

No. Digital loan origination automates repetitive, rule-based tasks — data entry, document verification, bureau pulls, and standard credit decisions — freeing your team to focus on complex cases, exceptions, and relationship management. Most lenders find that their teams become more productive and strategic after implementing digital origination, not redundant.

Q6: What loan products can be originated digitally?

Virtually any retail or MSME lending product can be originated digitally. Roopya supports 20+ pre-configured loan product journeys including personal loans, business loans, MSME credit lines, gold loans, home loans, microfinance (JLG) loans, payday loans, and vehicle loans. Each product type has a tailored application journey and underwriting workflow.

Q7: How does digital loan origination handle fraud detection?

Digital origination platforms use AI-powered document analysis to detect inconsistencies, anomalies, and fraud signals in uploaded documents — including bank statement manipulation, altered income proofs, and identity mismatches — with accuracy levels that routinely exceed what manual reviewers can achieve. Roopya's fraud detection layer runs automatically on every application.