If you have ever opened a bank account, applied for a home loan, or gone through any kind of financial onboarding in India, there is a good chance your information sits in a central registry you have never heard of. That registry is managed by CERSAI — and it plays a much bigger role in India's financial system than most people realise.

This article breaks down what CERSAI is, how it connects to CKYC, and why the whole system exists in the first place.

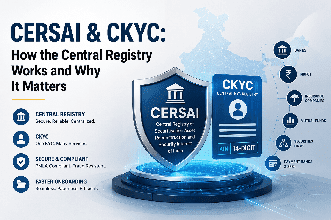

What Is CERSAI?

CERSAI stands for Central Registry of Securitisation Asset Reconstruction and Security Interest of India. It was set up in 2011 under the SARFAESI Act as a government company — jointly owned by the Central Government, public sector banks, and the National Housing Bank.

Its original job was to maintain a central record of mortgages and security interests on property. When you take a home loan and pledge your property as collateral, that pledge is supposed to be registered with CERSAI. This prevents a situation where someone takes multiple loans against the same property from different lenders — a form of fraud that was surprisingly common before CERSAI existed.

Over time, the government expanded CERSAI's responsibilities. Today, one of its most important functions is running the Central KYC Registry — the backbone of what we call CKYC.

So What Is CKYC?

CKYC — Central KYC — is a system where your KYC verification is done once and stored centrally. Any financial institution that needs to verify your identity can then fetch that record from the central registry, rather than asking you to submit documents all over again.

Think about how many times you have filled out KYC forms — for your bank, your mutual fund, your insurance policy, your demat account. With CKYC, ideally you do it once. You get a 14-digit KYC Identifier Number (KIN), and that number travels with you. Any regulated entity — bank, NBFC, insurance company, securities firm — can pull your verified record using that number.

The whole thing is governed by the Finance Ministry and executed through CERSAI, which acts as the central repository where all these records are stored and maintained.

Who Has to Follow CKYC Rules?

CKYC compliance is not optional for regulated financial institutions. Under the Prevention of Money Laundering Act (PMLA), the following types of entities are required to upload customer KYC data to the CKYC registry:

• Banks (scheduled commercial, cooperative, regional rural)

• Non-Banking Financial Companies (NBFCs)

• Insurance companies

• Mutual Funds and Asset Management Companies

• Securities brokers and depository participants

• Payment banks and small finance banks

These entities are referred to as Reporting Entities under PMLA. When they onboard a new customer, they are obligated to check whether a CKYC record already exists. If it does, they use it. If it does not, they create one and upload it.

How the CKYC Process Actually Works?

Here is the flow, step by step:

• Customer submits KYC documents: Identity proof, address proof, photograph, and PAN are collected during onboarding by a bank or financial institution.

• Institution verifies the documents: The reporting entity checks the documents and runs basic validation — often against government databases like UIDAI for Aadhaar or NSDL for PAN.

• Record is uploaded to CERSAI: The verified KYC data is pushed to the Central KYC Registry. The customer gets a 14-digit KIN.

• KIN is shared for future onboarding: The next time the customer approaches any regulated institution, they provide their KIN. The institution fetches the record directly from the registry — no fresh paperwork required.

• Updates flow back to the registry: If a customer updates their address or submits a new document, the reporting entity is supposed to push the updated record to CERSAI so the central file stays current.

Individual vs Legal Entity CKYC

CKYC was initially designed for individual customers — salaried employees, self-employed professionals, retail investors, and so on. But companies and corporates also engage with banks and financial institutions. They borrow money, open current accounts, and onboard as partners or merchants.

To cover this, CERSAI extended the CKYC framework to legal entities — private limited companies, LLPs, trusts, partnership firms, and more. The process is similar but involves additional documents: certificate of incorporation, PAN of the entity, details of beneficial owners who hold 25% or more stake, and authorisation letters. Legal entities also receive a 14-digit KIN, just like individuals.

How Financial Institutions Use the Registry Today

For a single branch handling a handful of customers a day, manually looking up CKYC records is manageable. But for banks and fintechs processing thousands of onboarding requests, that approach falls apart quickly. Most institutions today connect to the CERSAI registry through a CKYC API — a direct, real-time integration that lets their systems query the registry the moment a customer enters their KIN. Instead of someone manually logging into a portal, pulling a record, and re-entering it into a separate system, the whole thing happens automatically in the background. The customer barely notices. The compliance team gets a clean, verified record. And the institution stays on the right side of its regulatory obligations without slowing down its onboarding.

Why CERSAI and CKYC Matter Beyond Convenience

The convenience angle is obvious — doing KYC once instead of ten times is a genuine improvement for customers. But the deeper purpose of this system is financial security and fraud prevention.

Here is what the CKYC registry actually helps prevent:

• Identity fraud: Verified records mean it is much harder to use fake or altered documents to open accounts.

• Money laundering: PMLA compliance requires financial institutions to know who their customers actually are. CKYC makes that traceable.

• Duplicate records and data inconsistencies: A central registry means one authoritative record per customer, reducing the chaos of different institutions holding conflicting data.

• Shell company misuse: For legal entities, CKYC's beneficial ownership requirements make it harder for fraudulent or opaque structures to access financial services undetected.

Conclusion

CERSAI started as a mortgage registry and quietly became the backbone of India's KYC infrastructure. Today it sits at the centre of how banks, NBFCs, insurance companies, and financial platforms verify the people and businesses they deal with.

For customers — individuals and businesses alike — understanding CKYC means knowing that your KYC information has a permanent home in a central registry. You are not starting from scratch every time. For financial institutions, it means a standardised, auditable record that satisfies regulatory requirements and speeds up onboarding at the same time.

It is one of those systems that works quietly in the background — most people never interact with it directly. But it shapes nearly every financial relationship in the country.